As US factories are struggling to keep up with demand, it’s a now or never moment to make domestic manufacturing more competitive.

By Katy George and Eric Chewning

Manufacturing has been a staple of American prosperity for decades. The COVID-19 pandemic has underscored the industry’s critical role in fueling an economic recovery for working families , while providing products that are critical to health, safety, national security, and the continuity of multiple industries.

While US factory output increased in March by the most in eight months, continued supply-chain disruptions and shortages of goods from ketchup packets to semiconductor chips are constant reminders about why manufacturing matters. The consequences have also sparked an urgency to revitalize the US industrial base—an effort that would create new jobs, and the nation be more productive, competitive, and resilient.

Fragmented efforts to strengthen US manufacturing have not worked in the past, and they seem unlikely to achieve a broad manufacturing renaissance now. Nor do market forces appear able to solve the issue on their own. In the past decade, federal, state, and local governments have poured more than $85 billion into some 15,000 initiatives, such as business enticements, employment subsidies, and R&D incentives. The sheer range of these past efforts underscores the multifaceted nature of the challenge.

Accordingly, this moment calls for an ambitious, comprehensive plan, grounded in the competitive realities facing companies in different parts of the value chain. Since multiple interconnected issues affect manufacturing, they would need to be addressed in tandem. We have therefore identified five pillars that could help chart the path forward for revitalizing US manufacturing.

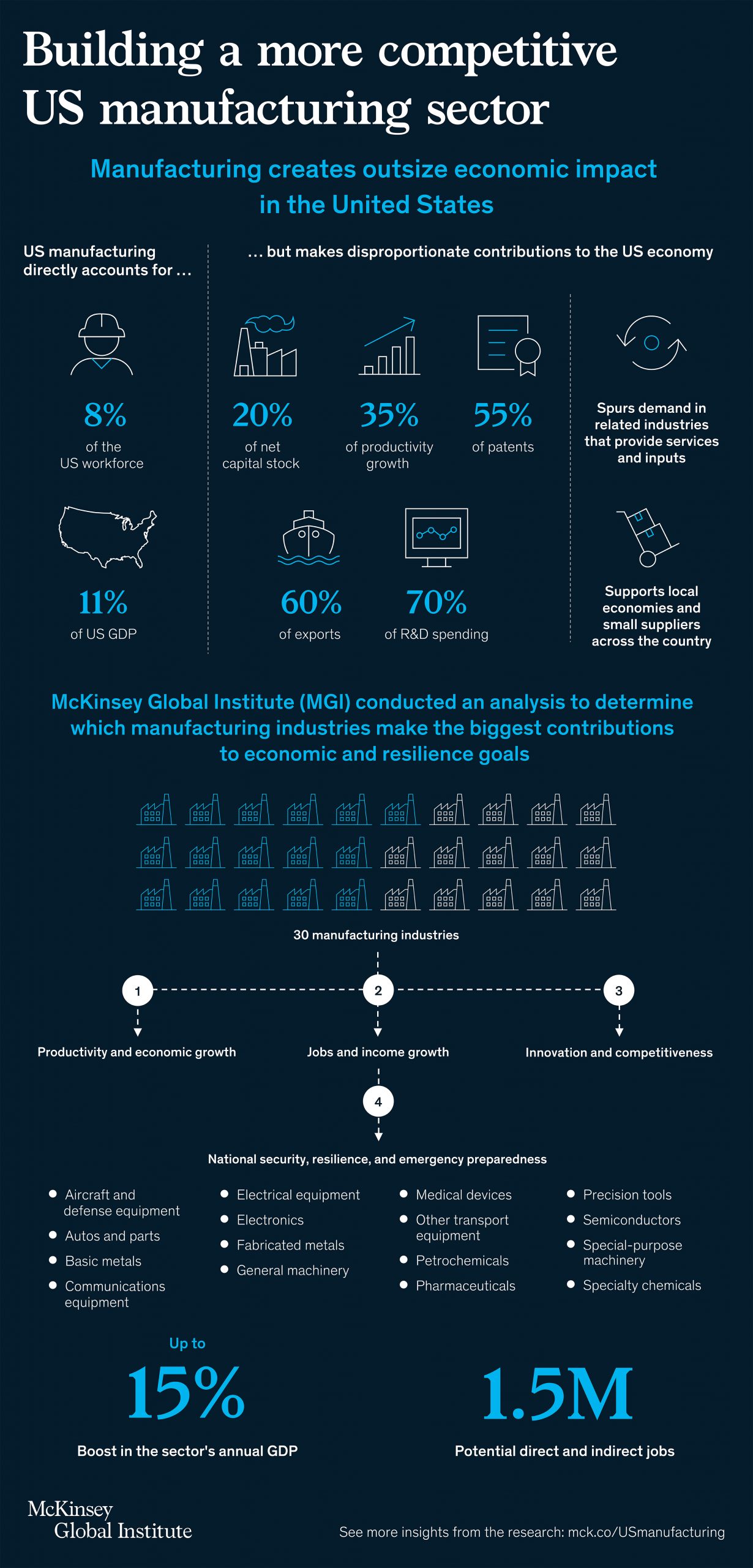

America’s manufacturing industry has declined over the past two decades—its global share has fallen from 25 to 17 percent since 1997, with the net loss of 4.6 million jobs. Yet the sector still represents 11 percent of US GDP and accounts for 30 percent of productivity growth, 60 percent of exports, and 70 percent of business R&D.

Starting from a list of 30 manufacturing industries, research from McKinsey Global Institute identifies 16 “key” sectors that can advance not only productivity and economic growth, but also jobs and incomes for workers and communities, along with innovation, competitiveness and national resilience. They range from precision tools to auto parts, and from pharmaceuticals and medical devices to semiconductors and communications equipment. With the right strategies, these 16 sectors could boost GDP by more than 15 percent ($460 billion) and add up to 1.5 million additional, well-paid jobs.

The potential benefits at stake are significant: new technologies, process innovations, input trends, and demand patterns are creating opportunities that did not exist even a decade ago—especially in key industries.

Any discussion of revitalizing US manufacturing in recent years has included the skills gap. Indeed, companies report difficulty filling open positions, with too few applicants or applicants who lack the necessary technical abilities.

The skill profiles of entire organizations are set to continue evolving. For example, advanced manufacturing roles that require a combination of deep domain expertise and digital skills—such as analytics translators or product owners—would change a company’s long-term talent strategy, necessitating the need for in-house capability building. Some companies are already tackling this issue in concert with industry groups and community colleges to create a pipeline for higher-level specialized skills.

The most successful manufacturing companies have defined learning journeys for different roles, and encourage employees to go above and beyond those journeys through continuous learning and exploration of areas of interest. Strategies like tiered pathways for upskilling ensure workers remain connected, integrated, and directly involved with transformations, while equipping workers with the expertise needed to contribute to future innovation.

Those US companies that succeed in upskilling are well positioned to lead in the even more important transformation of global manufacturing: the Fourth Industrial Revolution. No longer hype, the revolution is fully here, enabling real gains in productivity, sustainability, agility, and speed to market. Manufacturers that choose to reimagine their growth strategies by embracing the advances are setting new benchmarks. Those that do not risk falling behind in an uncertain and increasingly threatening competitive landscape.

We estimate that the United States needs to invest $15 billion to $25 billion a year for the next decade to upgrade aging plants and equipment. Modernizing existing plants and building new ones could draw much-needed investment into communities. Investing in new equipment and Industry 4.0 technologies is a critical part of this effort. For example, design and simulation tools can create “digital twins” of physical products and production processes to validate new design and process ideas in a low-risk way before they go live. New generations of sensors feed even larger quantities of real-time data into analytics systems, which can adjust machinery automatically to reduce downtime and waste.

Research estimates that there are roughly 25 percent fewer U.S. manufacturing firms and plants than there were in 1997. Increased import dependence has therefore left a range of strategic U.S. manufacturing supply chains exposed to shocks and disruptions. To mitigate risk exposure and the impact of disruptions, manufacturing needs a healthy domestic supplier base and more resilient supply-chain management to thrive.

For that to occur, the U.S. needs a targeted approach to help revitalize struggling small and midsize suppliers. The national conversation about manufacturing tends to focus on large, well-known companies, but the bulk of the production is done by the SMEs. Acutely focusing on them can improve the entire sector’s resilience and create more jobs. Large manufacturers could help make a difference. An important move would be to change incentive structures for their own purchasing teams. Instead of just monitoring key suppliers, OEMs could mentor them, solicit their ideas, invest in their capabilities, and build trust to create preferred relationships.

Focusing on productivity is not only about improvements on the factory floor, however. The public sector can also make the big long-term investments in infrastructure that support productivity in industry, such as transportation infrastructure, education and vocational training, digital networks, and energy.

The US can benefit from examining the range of active approaches to industrial support taken by peer countries and adapting some ideas to its own context. For example, Germany’s technical assistance program for small manufacturers is far larger and better funded than the comparable US federal program. Institutions such as Germany’s KfW or the Japan Finance Corporation expand local manufacturers’ access to long-term capital, but no similar public-sector entity provides support for US manufacturers.

Making US manufacturing more competitive would involve adding new capacity, upgrading existing plants and equipment, deploying new technologies, upgrading workforce skills, and setting off a virtuous cycle of import substitution. Capturing these opportunities will not be easy, and will likely take coordinated public- and private-sector efforts. The time to start is now.

About the Authors

Katy George is a Senior Partner at McKinsey & Company and leads the Operations Practice in North America, is a co-convener of the practice globally, and is a member of McKinsey’s Shareholders Council, the global governance board.

Eric Chewning is a partner in McKinsey’s Advanced Industries practice and specializes in issues at the intersection of national security, technology, and business.

Industry in Transition: The Forces Reshaping Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.