Learn how manufacturing businesses structure financing, meet lender requirements, and optimize capital stacks for growth and scalability.

By Christopher Cornella

Manufacturing financing is more complex because businesses require capital across equipment, inventory, real estate, and working capital simultaneously. Lenders prioritize cash flow stability and operational discipline over asset value alone. Companies with diversified customers and efficient operations are more likely to secure favorable terms and higher leverage capacity.

“Manufacturing financing succeeds or fails based on structure, not access to capital.”

— Industry Analysis

Modern manufacturing has evolved into a capital-intensive, technology-driven sector. Automation, reshoring, and supply chain optimization have increased efficiency while raising the need for more sophisticated financing structures.

Unlike service-based businesses, manufacturers must fund multiple operational layers simultaneously, including production equipment, raw materials, labor, and distribution. This creates constant liquidity pressure, making financing structure more important than loan size alone.

Most manufacturing transactions rely on multiple funding sources working together.

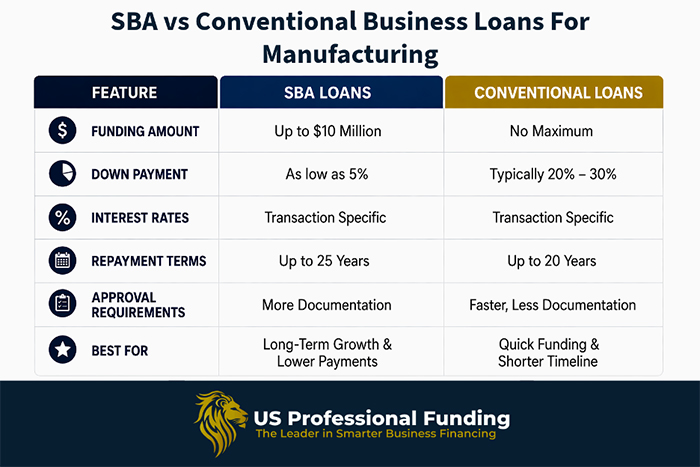

SBA 7(a) loans support acquisitions, working capital, and equipment financing with funding up to $5 million. SBA 504 loans are commonly used for real estate and large equipment purchases with long-term fixed structures.

Banks provide term loans and revolving credit facilities, but require strong financial performance, stable cash flow, and conservative leverage levels.

Equipment can be financed as part of a broader loan or through standalone leases and term loans aligned with asset life cycles.

Manufacturers rely heavily on revolving credit facilities secured by receivables and inventory to manage production cycles and cash flow timing.

Private equity or strategic investors are often used for acquisitions, expansion, or scaling initiatives. This reduces leverage but dilutes ownership.

Common in acquisitions, seller notes bridge valuation gaps and improve deal flexibility while aligning buyer and seller incentives.

Lenders focus on EBITDA consistency, margins, and debt service coverage ratios to determine repayment capacity.

A diversified customer base reduces revenue risk. High concentration increases underwriting scrutiny.

Modern, well-maintained machinery improves productivity and strengthens collateral value.

Efficient inventory turnover and reliable suppliers signal operational discipline and reduce risk exposure.

Strong leadership with industry expertise is often a deciding factor in approval decisions.

According to the National Association of Manufacturers, manufacturing represents approximately 11% of U.S. GDP, making it one of the most critical sectors for commercial lending activity.

SBA 7(a) loans can provide up to $5 million in financing, making them one of the most widely used funding tools for small and mid-sized manufacturers.

Typically easier to finance due to established cash flow. Structures often include SBA loans, senior bank debt, seller financing, and equity contributions.

Used for scaling production capacity, upgrading equipment, or improving efficiency. Funded through a mix of term loans, equipment financing, and working capital lines.

Higher-risk projects requiring construction financing, SBA 504 loans, and significant equity. Lenders place heavy emphasis on feasibility and projections.

Manufacturers require capital across multiple asset types simultaneously, increasing structuring complexity and lender scrutiny.

Consistent cash flow and strong debt service coverage are the most important underwriting factors.

SBA loans, conventional bank loans, equipment financing, and revolving credit facilities.

Industries with stable demand, automation integration, and strong margins tend to attract the most capital.

Manufacturing financing is fundamentally about structure, not just access to capital. Companies that align financing tools with operational needs gain stronger liquidity, lower risk exposure, and greater scalability. As the industry continues to evolve, capital efficiency will remain a key competitive advantage.

About the Author:

Christopher Cornella is VP of Business Development at US Professional Funding, specializing in structured financing solutions for manufacturing and industrial businesses. He works with operators and investors to optimize capital structures for growth and acquisitions.

Read more from the author:

How Car Wash Owners Are Financing Multi-Site Growth (2026) | CarWashBiz, April 2026

How Car Wash Owners Are Financing Multi-Site Growth in Today’s Market (2026) | Heartland Carwash Association, April 2026

Forging the Next 250 Years: Powering the Next Era of American Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.