Most manufacturers know Mexico is cost-competitive. Few know by how much, or that location within Mexico changes the entire equation.

By: Doug Donahue, Co-Managing Partner, Entrada Group

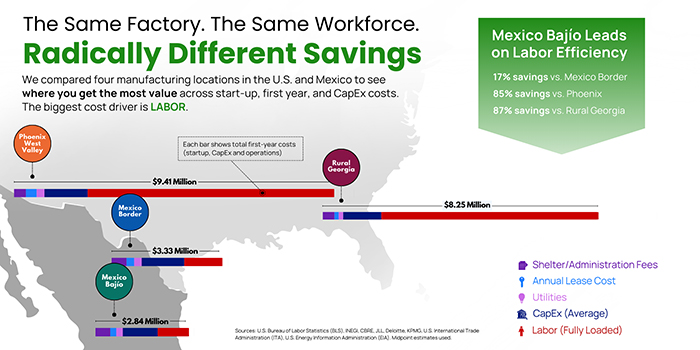

A 100-person manufacturing operation in Phoenix, Arizona costs $9.41 million in its first year. The same facility, same workforce, same production output, located in Mexico’s Bajío region, costs $2.84 million. That’s a 70% difference in year-one costs. For manufacturers who have thought about Mexico but haven’t looked closely at where in Mexico, and why that location matters, those numbers deserve a closer look.

Most manufacturers already understand that Mexico offers cost-competitive operations compared to the U.S. What’s less understood is the magnitude of that advantage in practice, and how significantly it varies depending on which part of Mexico you’re operating in. The border cities that many companies think of first look very different, cost-wise, from the country’s industrial interior. Mexico is not one manufacturing market. It’s several, and choosing the right one matters more than most people realize.

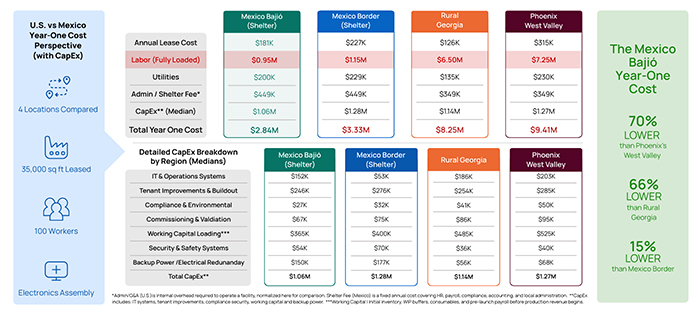

To put real numbers behind that difference, we built a cost model from publicly available data, drawing from the U.S. Bureau of Labor Statistics, Mexico’s INEGI, CBRE, JLL, Deloitte, KPMG and the U.S. International Trade Administration. The scenario was consistent across all four locations: a 35,000-square-foot facility with 100 workers, covering all startup and first-year costs. Electronics assembly served as the baseline, but the cost drivers hold reliably across most manufacturing categories, from wire harnesses and automotive components to medical devices and industrial machinery.

The U.S. locations were chosen as fair benchmarks. Rural Georgia represents one of the more cost-competitive domestic manufacturing environments available. Phoenix’s West Valley is an actively growing electronics and industrial hub, with incentive programs specifically targeting that sector.

The Mexico Bajío, the country’s central manufacturing corridor anchored by states including Guanajuato and Zacatecas, came in at $2.84 million for year one. Phoenix, Arizona: $9.41 million. Rural Georgia: $8.25 million. Mexico’s border region: $3.33 million, still 17% higher than the Bajío.

The gap between Mexico’s interior and either U.S. location is significant enough to reshape a business case entirely. At 70% below Phoenix and 66% below rural Georgia, the Bajío’s cost profile doesn’t just affect operating margins and profitability. It changes what a manufacturer can afford to invest next and how competitively they can price their product in the market.

That labor is the dominant cost driver won’t surprise anyone in manufacturing. What the model makes concrete is how extreme the cost-competitiveness advantage actually is in practice.

In the Bajío, fully loaded labor for 100 workers costs approximately $950,000 for the year. In Phoenix, that same workforce costs $7.25 million. Lease rates, utilities and CapEx are relatively close across all four locations. Labor is not.

Mexico’s manufacturing wages have risen meaningfully over the past five years, with annual increases varying between 10 and 20 percent depending on region and sector. That trend is real and worth factoring into any long-term planning. But even with that trajectory, Mexico’s cost-competitive labor position remains a fraction of U.S. rates. The relationship between the two is less like a narrowing gap and more like comparing pennies to dollars.

Part of what sustains that difference is structural. The U.S. faces well-documented labor shortages in manufacturing, driven by an aging workforce and a long-term contraction in the available industrial labor pool. Mexico, by contrast, has a young, growing population where manufacturing is still an appealing and stable career path. That demographic reality supports both workforce availability and cost stability in ways that are difficult to replicate in most alternative production locations.

The assumption that nearshore means border is one of the more costly misconceptions in Mexico manufacturing strategy. Competition for workers in border cities like Monterrey, Tijuana or Ciudad Juárez is intense, and wages there have climbed sharply in recent years. In some border states, annual minimum wage increases have run at roughly double the rate seen in Mexico’s interior. The cost-competitive advantage that draws manufacturers to Mexico in the first place is significantly reduced when you’re operating near the border. Labor costs there can run as much as 50% higher than in the Bajío.

Distance from the border is not a logistical weakness. For a workforce that is deep, industrially experienced and cost-competitive, it’s a structural advantage. The state of Guanajuato alone has more than 627,000 people employed in industrial manufacturing, representing 24% of the total state workforce, a labor market built over decades of automotive, aerospace and electronics investment.

A cost model captures medians. It doesn’t capture what happens once you’re actually operating.

Turnover is one clear example. The model assumes a stable workforce. It doesn’t price in replacement costs, productivity drops during transitions, or the management overhead of constant onboarding. Even in a favorable labor market, retention has a direct and measurable impact on your actual cost structure.

Setup costs are another area the model captures only partially. One factor that genuinely changes the math for smaller and mid-sized manufacturers is Mexico’s shelter services model, a structure without a direct equivalent in most other manufacturing destinations. A shelter provider like Entrada Group operates as an established legal entity in Mexico, with compliance infrastructure, HR, accounting and customs management already in place. A manufacturer can enter within that structure without building a Mexican subsidiary from scratch.

In most other countries, establishing manufacturing operations abroad requires the resources of a large multinational. The shelter model makes Mexico’s cost-competitive environment accessible to a company with 50 or 200 employees, with a manageable upfront investment and a significantly shorter path to first production.

USMCA, the free trade agreement governing commerce between the U.S., Mexico and Canada, is scheduled for its mandatory review in 2026. If no changes are made, it automatically remains in force for another ten years. Even in a renegotiation scenario, the foundational trade relationship between the two countries is too deeply integrated for any outcome that fundamentally disrupts it.

Within that framework, goods manufactured in Mexico and shipped to the U.S. move duty-free when rules of origin requirements are met. The IMMEX program allows duty-free import of raw materials for export-bound production. Compared to manufacturing in Asia or virtually any other region outside North America, Mexico’s trade position sits in a different category. Tariff exposure from Asian production locations runs dramatically higher, with no equivalent agreement providing the built-in duty protection that USMCA delivers. That difference compounds over time and belongs in any honest cost comparison.

This model is built from publicly available data using industry medians. For highly labor-intensive manufacturing operations, the real cost-competitiveness advantage in Mexico may run considerably higher than what this comparison shows. When labor represents a larger share of total cost, the per-worker differential compounds more sharply and the Bajío advantage becomes even more pronounced.

The most useful version of this analysis is one built against your own operation: your workforce profile, your facility requirements, your bill of materials and your production volume. A model built on public data gives you a directional answer. Getting to a real business case means working with a partner who understands what those inputs mean on the ground in Mexico, and who can build a cost model around your specific numbers rather than industry averages.

For the full line-by-line breakdown across all four locations, including the detailed CapEx comparison by region, the complete analysis is here on the Entrada Group website.

Interested in your own Mexico production facility? Join our monthly webinar to examine the first steps.

About the Author:

Doug Donahue is Co-Managing Partner of Entrada Group, a shelter services provider with over 20 years of experience guiding global manufacturers through the setup and operation of production facilities in Mexico. Entrada operates manufacturing campuses in Zacatecas and Celaya, Guanajuato, and manages trade compliance, HR, legal and accounting services for client operations across multiple industries.

Read more from the author:

Electronics Manufacturers Can’t Compete without Mexico | Industry Today, August 14, 2018

Medical Device Manufacturers Looking To Move Production From China Have Options | Forbes, November 15, 2022

Forging the Next 250 Years: Powering the Next Era of American Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.