New research shows industry leaders are optimistic about growth, even as cyber risk, talent and AI readiness top their agenda of priorities.

Leaders in the manufacturing and distribution industry are looking ahead with renewed confidence, even in the face of some significant market and geopolitical headwinds. Results of recent global research among board members and C-suite executives show optimism about near-term growth opportunities, even as cyber risk, talent shortages and the accelerating adoption of AI present complex challenges. The message is clear: Organizations that modernize, secure their operations, and prepare their workforce for AI adoption and broader technology transformation will be best positioned to turn uncertainty into opportunity.

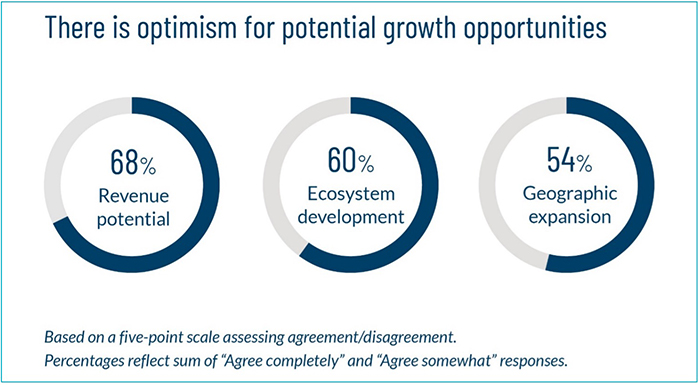

The results of the survey indicate that leaders in the manufacturing and distribution sector are optimistic about the next two to three years, despite recent periods of economic uncertainty and tariff-driven headwinds.

While this study was conducted prior to the conflicts in Iran and the Middle East that erupted in February this year, several longer-term factors underpin the confidence of boards and executives. Among them, infrastructure development continues to drive demand across many industries, offering significant opportunities for manufacturers to expand capacity, capture new markets and grow revenue. Tariffs remain a concern given continued volatility in policymaking. Yet even amid these challenges, there is renewed optimism among industry leaders in light of opportunities around regional reindustrialization and supply chain diversification.

These leaders also see AI-driven solutions as a game changer, offering the promise of improvements in areas such as predictive maintenance, process automation and enhanced decision-making. Organizations investing in Industry 4.0 technologies can realize transformative payoffs by reducing downtime, boosting efficiency and accelerating innovation.

AI-driven modernization and collaborative ecosystems position manufacturing and distribution companies to move beyond recent stagnation and capitalize on a wave of global growth that’s anticipated over the next two to three years. They need to invest in technology, partnerships and capacity to seize these growth opportunities and secure their long-term competitiveness.

AI promises transformative gains in efficiency and innovation, yet its practical integration into manufacturing and distribution environments remains a complex endeavor.

One significant hurdle: Years of underinvestment in integrated systems have left many manufacturers wrestling with siloed data and legacy infrastructure that limit how quickly AI can be deployed at scale. These issues call for sustained coordination, capital commitment and a willingness to modernize how data flows across the enterprise.

These challenges are compounded by workforce readiness. Employee concerns remain a genuine barrier, with many wary of how AI will reshape their roles, careers and long-standing ways of working. Equipping employees to realize AI’s value will demand sustained investment in training and a focus on building a culture that embraces change while supporting the workforce.

Then there are competitive pressures. Compared with more digitally native sectors, manufacturing has often moved at a slower pace when adopting emerging technologies. The inability to deploy AI solutions rapidly and effectively could erode market position.

Cybersecurity is another critical AI challenge, considering that manufacturing and operational technology environments are prime targets for ransomware attacks. As AI becomes more deeply embedded in operations, it can also widen the attack surface, particularly in environments where IT and OT are intertwined. Manufacturers must weigh AI’s benefits against heightened security risks.

Volatility in global markets and trade policies continues to dominate the near-term risk outlook for manufacturing and distribution leaders. Uncertainty resulting from changing government policies around the world (such as U.S. administration-driven tariffs) are fueling these concerns given the global nature of manufacturing operations and their complex supply chains. Recent developments in Iran and the Middle East are further exacerbating these concerns.

A tight labor market, rising costs and impending “peak retirements” are also concerning, as these issues threaten workforce stability. Even as AI and technology transformation creates shifts in talent models and organizational structures, a quarter of the workforce is age 55 or older. With millions of roles projected to open by 2033 due to retirements, manufacturing and distribution companies must compete aggressively for talent while adapting to evolving skill requirements driven by Industry 4.0 and AI integration. These challenges are amplified by the industry’s footprint, with many operations located far from urban centers with the deepest labor pools.

On the cyber front, high-profile incidents involving a number of well-known manufacturers call out the vulnerability of production systems and supply chains. As digital and operational systems become more tightly connected, manufacturers are contending with a broader and more complex cyber risk profile, and 88% of organizations with industrial environments struggle with detection and response, according to research from Dragos. And as noted earlier, AI adoption is introducing further challenges in terms of cybersecurity, operational continuity and data integrity.

Looking further ahead, industry executives expect the risk conversation to evolve beyond plant-level issues toward questions of strategy, competition and market relevance. In the eyes of boards and executives, competitive differentiation is critical in an industry known for commoditization. This shift is evident in growing efforts to move beyond transactional B2B models toward more customer-centric, experience-driven approaches. For these industry leaders, long-term success hinges on the organization’s ability to leverage technology, personalize offerings and innovate to create unique value propositions for the client and customer.

Challenges around talent and access to the right skills will continue as well. Recruiting and retaining talent, together with upskilling and reskilling employees, will remain persistent long-term concerns.

The long-term risk outlook indicates that manufacturing and distribution organizations which embrace AI-driven innovation and differentiate themselves in a dynamic global environment will thrive. Those that remain saddled to legacy infrastructure and traditional operating and talent models that hinder agility, customer focus and resilience risk becoming irrelevant.

Given these broad near- and long-term priorities and challenges, what are some steps manufacturing and distribution leaders need to take to address them? Here are some calls to action for them as they navigate the current environment and prepare for the future.

About the author

David Kupinski is a Managing Director and global leader of the firm’s Manufacturing and Distribution industry practice. He has over 25 years of experience in delivering tailored business solutions to his clients. Leveraging technology enablement, data analytics and internal controls, he works with finance executives to drive transformation through initiatives such as ERP implementation, shared service center strategies and finance process optimization.

Read more:

Industry 4.0 and beyond: Addressing cyber, talent and AI opportunities in manufacturing and distribution, January 2026

Transforming the Enterprise: How to Guide an ERP Implementation to Success

Forging the Next 250 Years: Powering the Next Era of American Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.