Organizations are no longer being separated by whether they plan for disruption. They’re being separated by how they execute when it happens.

By Richard Cooper, SVP of Global Market Transformation, Fusion Risk Management

Over the last decade, organizations invested heavily in automation, digital operations, cloud platforms, and supply chain modernization. But many resilience programs evolved separately from those operational systems.

That gap is becoming harder to ignore.

Fusion Risk Management’s Enterprise Resilience Report: 5 Years of Market Signals, based on 4,571 structured conversations across 1,765 organizations in manufacturing, financial services, insurance, life sciences, and retail, shows a market increasingly splitting into two groups. Some organizations are building real operational capability through automation, cross-functional visibility, and coordinated response. Others are still relying on static documentation, manual processes, and fragmented systems while operational complexity continues to increase.

That distinction matters because resilience is no longer measured by whether plans exist. It shows up in how quickly teams can respond, how clearly leaders can see risk, and how confidently organizations can demonstrate performance under pressure.

Most organizations already have plans across business continuity, disaster recovery, supply chains/third parties and compliance. However, many of those plans remain static and disconnected from how the business actually operates today.

At the same time, disruption itself has changed. Organizations now operate through increasingly interconnected systems shaped by AI acceleration, third-party dependencies, SaaS concentration, regulatory scrutiny, and cross-functional operational complexity.

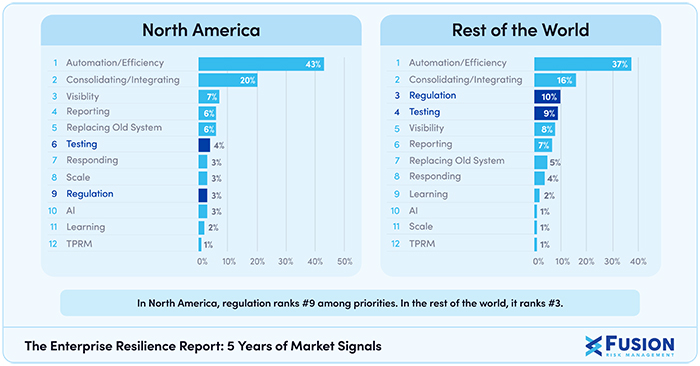

That pressure is accelerating globally. In North America, regulation accounted for just 3% of resilience priorities discussed in the report, compared to 10% in the rest of the world, reflecting growing influence from frameworks like DORA and rising regulatory scrutiny globally.

Disruptions also rarely stay contained. A supplier issue no longer affects only procurement. A SaaS outage can disrupt multiple business functions simultaneously. A cyber event can quickly escalate into a broader operational issue.

What once sat primarily within business continuity now spans crisis management, disaster recovery, third-party risk, executive governance, and operational decision-making.

Many resilience programs still operate through static documentation, spreadsheets, shared drives, and disconnected workflows. In fact, according to the report findings, visibility and compliance concerns remained remarkably consistent from 2021 through 2025, even as organizations increased investment in resilience modernization and automation initiatives.

The problem is that risk today no longer exists in isolated silos. It moves across systems, suppliers, third parties, logistics networks, and geographies simultaneously. Organizations cannot coordinate effectively during disruption if they cannot see clearly across those operational dependencies.

In practice, response teams are often forced to manually assemble information during incidents, pulling from an ever growing set of disconnected data sources to understand operational impact, recovery priorities, and downstream exposure. As disruptions become more interconnected, those delays become increasingly costly.

One of the clearest shifts in the data is how organizations are approaching resilience investment. For years, resilience conversations focused primarily on integration and consolidation — connecting systems, reducing silos, and improving consistency across programs. But in 2024 and 2025, automation and efficiency overtook integration as the top priority. Across every region tracked, automation and efficiency emerged as the leading resilience priority, representing 43% of resilience priorities discussed in North America and 37% in the rest of the world.

That shift reflects a broader operational reality. Integration helped organizations reduce fragmentation, but automation is increasingly becoming the mechanism for scaling response, testing, evidence collection, and operational coordination as complexity continues to grow.

Organizations are now trying to expand testing, reporting, and coordinated response capabilities without increasing operational overhead at the same rate. The organizations performing best during disruption are often the ones that have already worked through operational tradeoffs ahead of time and understand where dependencies create downstream impact.

As a result, the organizations making the most progress are embedding resilience directly into operational infrastructure rather than treating it as a separate compliance exercise. The shift is from compliance to operating capability.

Manual tools remain deeply embedded across resilience programs. Across the conversations analyzed for the report, 70% of organizations cited challenges tied to spreadsheets, shared drives, and other fragmented workflows.

The issue is no longer simply inefficiency. When operational data remains fragmented, the gap between what organizations publicly communicate about resilience and what they can operationally support becomes more visible.

The organizations performing best are not necessarily avoiding disruption. They are the ones responding rapidly with greater visibility, coordination, and confidence when disruption occurs.

At a high level, the takeaway is simple: organizations are no longer being separated by whether they plan for disruption. They’re being separated by how they execute when it happens.

About the Author:

Rich Cooper is a global risk and resilience executive and Global Head of Market Transformation at Fusion Risk Management, where he helps organizations strengthen operational resilience and navigate complex disruption scenarios. He works with global enterprises across industries to understand operational dependencies and sustain critical operations during disruption.

Forging the Next 250 Years: Powering the Next Era of American Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.