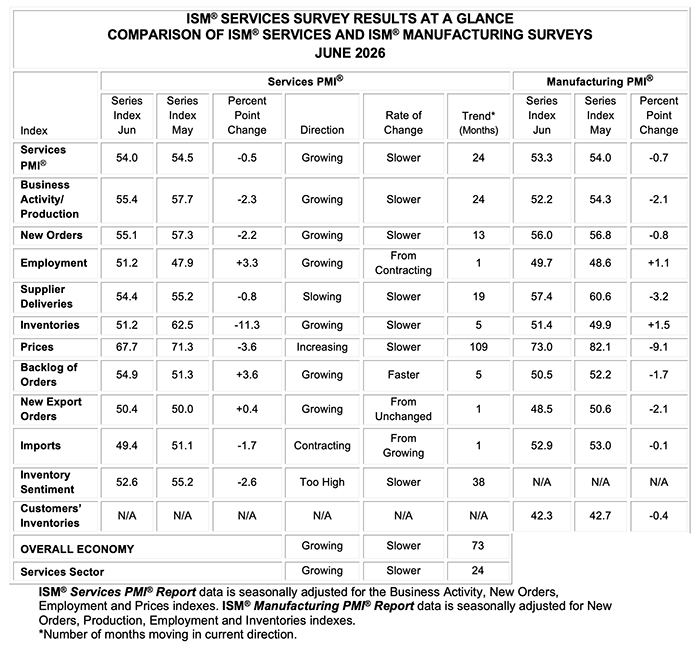

Economic activity in the services sector continued to expand in June, say the nation’s purchasing and supply executives in the latest ISM® Services PMI® Report.

Services PMI® at 54%

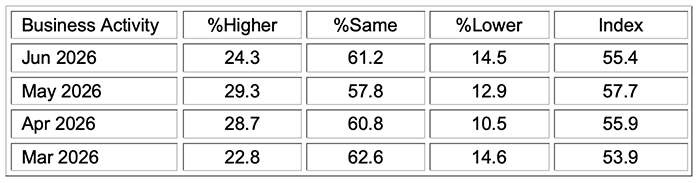

Business Activity Index at 55.4%

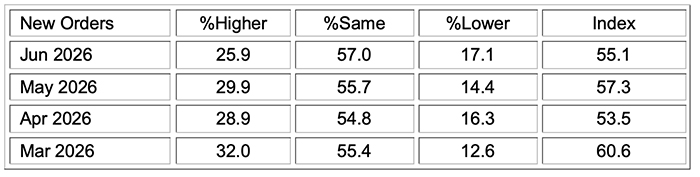

New Orders Index at 55.1%

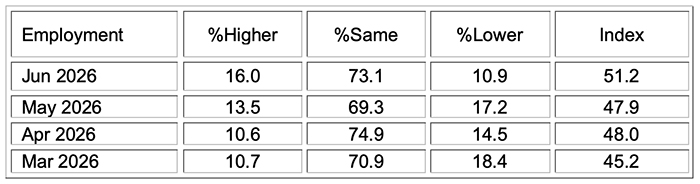

Employment Index at 51.2%

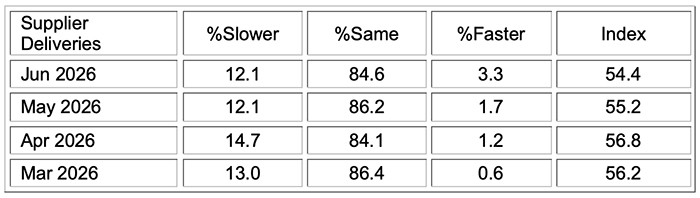

Supplier Deliveries Index at 54.4%

(Tempe, Arizona) — The Services PMI® registered 54 percent, the 24th consecutive month in expansion territory.

The report was issued today by Steve Miller, CPSM, CSCP, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee: “In June, the Services PMI® registered 54 percent, a decrease of 0.5 percentage point compared to May’s figure of 54.5 percent. The Business Activity Index remained in expansion territory in June, decreasing 2.3 percentage points to 55.4 percent from May’s reading of 57.7 percent. The New Orders Index registered 55.1 percent, 2.2 percentage points below May’s figure of 57.3 percent. The Employment Index expanded for the first time in four months with a reading of 51.2 percent, a 3.3-percentage point increase from the 47.9 percent recorded in May. All of the four subindexes that make up the composite PMI® were above their 12-month moving averages,” says Miller.

“The Supplier Deliveries Index registered 54.4 percent, 0.8 percentage point lower than the 55.2 percent recorded in May. This is the 19th consecutive month that the index has been in expansion territory, indicating slower supplier delivery performance. (Supplier Deliveries is the only ISM® PMI® Reports index that is inversed; a reading of above 50 percent indicates slower deliveries, which is typical as the economy improves and customer demand increases.)

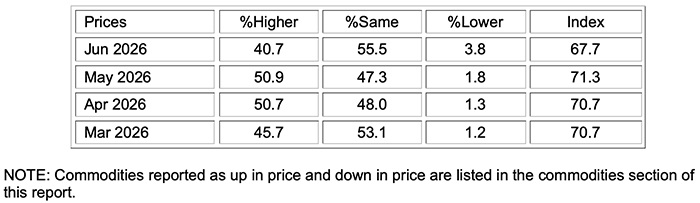

“The Prices Index decreased to 67.7 percent in June, 3.6 percentage points below May’s figure of 71.3 percent and its first time below 70 percent since February. The index has exceeded 60 percent for 19 straight months, maintaining its 12-month average of 68 percent. Diesel, gasoline, oil and related commodities were once again most frequently mentioned as up in price in June — and cited as down in price from other respondents. This is likely due to different contract terms for these commodities between companies.

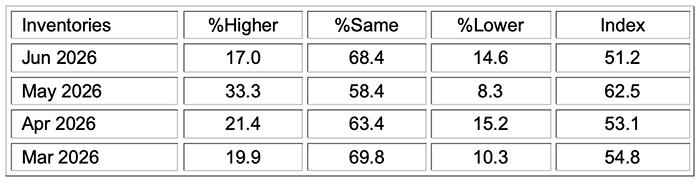

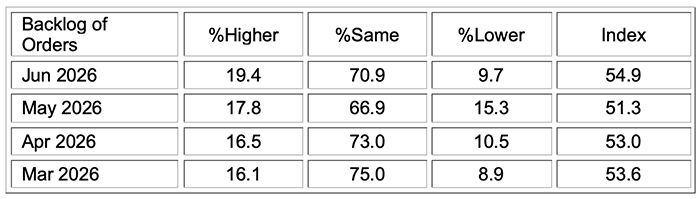

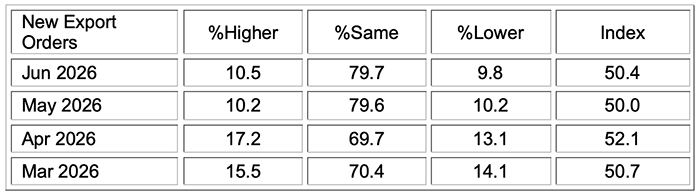

“The Inventories Index registered 51.2 percent, down 11.3 percentage points from May’s figure of 62.5 percent. The Inventory Sentiment Index expanded for the 38th consecutive month, registering 52.6 percent, down 2.6 percentage points from May’s figure of 55.2 percent. The Backlog of Orders Index remained in expansion territory for a fifth straight month, increasing 3.6 percentage points to 54.9 percent in June from May’s reading of 51.3 percent. The New Export Orders remained at 50 percent or above for the fifth month in a row, increasing 0.4 percentage point in June, to 50.4 percent. The Imports Index dropped into contraction territory at 49.4 percent in June, a decrease of 1.7 percentage points compared to its May reading of 51.1 percent, and its third consecutive lower reading since reaching 55.2 percent in March.

“Fourteen industries reported growth in June, three less than in May, and the number reporting contraction were four, an increase of three from May. The June Services PMI® reading of 54 percent is 0.9 percentage point above the 12-month average of 53.1 percent. For the sixth straight month, that figure increased, with an uptick of 0.3 percentage point over May’s 12-month average of 52.8 percent.”

Miller continues, “The Prices Index decreased to 67.7 percent, its lowest reading since February 2026 (63 percent). In this month’s report, some respondents reported reduced prices paid for gasoline and diesel, but this was not seen across the board. Petroleum-related products were mentioned again as a commodity up in price, something that we expect to see for several months as higher oil prices work their way through the supply chain, but they should ease off in the fall assuming recent progress in moving oil through the Strait of Hormuz continues. As of late June, West Texas Intermediate crude oil dropped below US$70 per barrel for the first time since February, a more than 30 percent drop from its high in recent months. The Supplier Deliveries Index continued to indicate slower performance; while easing for its second month in a row, it is still above its 12-month average.

“The more than 2-percentage point drops in both the Business Activity and New Orders indexes were partially offset by the 3.3 percentage point increase in the Employment Index. All four subindexes of the Services PMI® are once again in expansion territory and above their 12-month averages. In a welcome sign of reduced growth rate of prices paid, June’s Prices Index reading of 67.7 percent is its lowest in four months and below its 12-month average. There were fewer commodities reported as up in price compared to previous months.

“Despite easing of the Supplier Deliveries Index, there was an increase in commodities listed as ‘in Short Supply,’ increasing from five in May to nine in June. All commodities in short supply in June are commodities necessary for data center construction, while the Utilities and Information industries all continued their more than six-month runs in expansion territory. Memory components, copper, aluminum, and heating, ventilation and air conditioning (HVAC) equipment continued multimonth runs of being listed as up in price.

“Respondents in June commented less frequently about pricing impacts on petroleum products, while tariff impacts continued to be a theme for increased pricing pressure. The Inventories Index dropped to its second-lowest level since October 2025, indicating that the buy-ahead phenomenon from earlier in the year may be over. The Imports Index dropped into contraction territory for the first time in five months, down from a spike to 55.2 percent in March, its highest level in over two years. The Backlog of Orders Index reached its second-highest level in almost four years. These readings, taken with respondent commentary, seem to indicate that supply chains are stabilizing amid sustained business activity, giving confidence to businesses that selective, yet modest, increased employment is warranted. World Cup-related hiring in the U.S. likely contributed to the increase to the Employment Index. Of the 18 services industries, nine of them — representing over 58 percent of U.S. gross domestic product (GDP) — reported higher employment levels in June. This represents widespread confidence that hiring is again warranted to support activity levels.”

The 14 services industries reporting growth in June — listed in order — are: Arts, Entertainment & Recreation; Mining; Wholesale Trade; Transportation & Warehousing; Finance & Insurance; Accommodation & Food Services; Retail Trade; Other Services; Professional, Scientific & Technical Services; Health Care & Social Assistance; Information; Construction; Utilities; and Real Estate, Rental & Leasing. The four industries reporting a contraction in the month of June are: Agriculture, Forestry, Fishing & Hunting; Educational Services; Management of Companies & Support Services; and Public Administration.

Aluminum (4); Aluminum Products; Beef; Computers and Related Items (2); Conductor Cable; Copper (7); Diesel* (4); Electrical Components; Food Products (2); Fuel* (5); Gasoline* (5); Heating, Ventilation and Air Conditioning (HVAC) Equipment (2); House Wraps; Insurance (2); Labor (11); Labor — Consulting; Labor — Technical; Lumber; Lumber — Plywood; Memory Products (6); Oriented Strand Board (OSB); Petroleum Based Products (2); Plastics; Software — Licensing (5); Software — Maintenance/Support (3); Soybean Oil (2); Steel Products (3); and Transportation (4).

Diesel*; Fuel*; and Gasoline*.

Computers and Related Items (2); Electronic Components (5); Labor; Memory Components (6); Software Licensing; Steel Products; Switchgear; Transformers; and Wire and Cable.

Note: The number of consecutive months the commodity is listed is indicated after each item.

*Indicates both up and down in price.

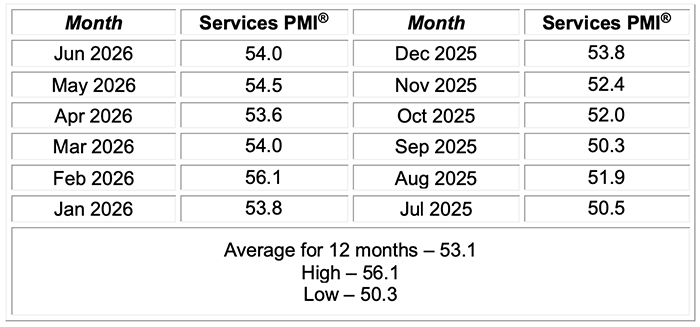

In June, the Services PMI® registered 54 percent, 0.9 percentage point above its 12-month moving average of 53.1 percent. A reading above 50 percent indicates the services sector economy is generally expanding; below 50 percent indicates it is generally contracting.

A Services PMI® above 48.1 percent, over time, generally indicates an expansion of the overall economy. Therefore, the June Services PMI® indicates the overall economy is expanding for the 73rd straight month. Miller says, “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for June (54 percent) corresponds to a 1.9-percentage point increase in real gross domestic product (GDP) on an annualized basis.”

ISM®’s Business Activity Index continued in expansion in June; the reading of 55.4 percent is 2.3 percentage points lower than the 57.7 percent recorded in May. June’s reading is 0.3 percentage point above its 12-month moving average of 55.1 percent. Comments from respondents include: “World Cup activity in the Dallas-Fort Worth (DFW) metroplex” and “Activity has been high for the past couple of years, given many electric industry new initiatives and projects.”

The 13 industries reporting an increase in business activity for the month of June — listed in order — are: Arts, Entertainment & Recreation; Retail Trade; Finance & Insurance; Transportation & Warehousing; Wholesale Trade; Mining; Other Services; Information; Accommodation & Food Services; Professional, Scientific & Technical Services; Utilities; Health Care & Social Assistance; and Real Estate, Rental & Leasing. The four industries reporting a decrease in business activity in the month of June are: Agriculture, Forestry, Fishing & Hunting; Management of Companies & Support Services; Public Administration; and Construction.

ISM®’s New Orders Index remained in expansion territory at 55.1 percent in June, 2.2 percentage points lower than the reading of 57.3 percent in May. The index has expanded for 13 consecutive months. Comments from respondents include: “Slightly higher in the last month with inventory, suppliers and contractors ready for the summer rush and any possible storms that affect the area” and “Volume is unfavorable to budget; other consumer expenses going up may be causing people to defer health-care spending.”

The 12 industries reporting an increase in new orders for the month of June — listed in order — are: Mining; Arts, Entertainment & Recreation; Transportation & Warehousing; Wholesale Trade; Finance & Insurance; Other Services; Real Estate, Rental & Leasing; Accommodation & Food Services; Professional, Scientific & Technical Services; Information; Utilities; and Retail Trade. The four industries reporting a decrease in new orders in the month of June are: Agriculture, Forestry, Fishing & Hunting; Management of Companies & Support Services; Construction; and Educational Services.

Employment activity in the services sector returned to expansion; the index registered 51.2 percent in June after three months in contraction. The reading is up 3.3 percentage points from the May figure of 47.9 percent and 2.5 percentage points above its 12-month average of 48.7 percent. Comments from respondents include: “Even though student population is down, we do not lay off staff for the summer — we actually hire counselors and sports camp directors, as we have several camps and youth conferences on campus” and “Summer interns hired.”

The nine industries reporting an increase in employment in June — listed in order — are: Retail Trade; Construction; Professional, Scientific & Technical Services; Accommodation & Food Services; Finance & Insurance; Wholesale Trade; Transportation & Warehousing; Health Care & Social Assistance; and Real Estate, Rental & Leasing. The five industries reporting a decrease in employment in June are: Agriculture, Forestry, Fishing & Hunting; Information; Educational Services; Public Administration; and Utilities.

In June, the Supplier Deliveries Index indicated slower performance for the 19th month in a row. The index registered 54.4 percent, down 0.8 percentage point from the 55.2 percent recorded in May. A reading above 50 percent indicates slower deliveries, while a reading below 50 percent indicates faster deliveries. Comments from respondents include: “Omani supplier lead times normalizing, Strait of Hormuz reopened and regional logistics stabilizing” and “Data-center flange (large diameter) lead times are getting much longer as demand outpaces supply.”

The 14 industries reporting slower deliveries in June — in the following order — are: Agriculture, Forestry, Fishing & Hunting; Mining; Wholesale Trade; Health Care & Social Assistance; Other Services; Accommodation & Food Services; Information; Transportation & Warehousing; Management of Companies & Support Services; Construction; Public Administration; Professional, Scientific & Technical Services; Finance & Insurance; and Educational Services. The two industries reporting a decrease in employment in June are: Real Estate, Rental & Leasing; and Utilities.

The Inventories Index expanded for the fifth month in a row, registering 51.2 percent, an 11.3-percentage point decrease compared to the 62.5 percent reported in May. Of the total respondents in June, 27 percent indicated they do not have inventories or do not measure them. Comments from respondents include: “Incrementally higher due to capacity planned items with suppliers, causing us to have more on hand for future needs” and “Getting ready for annual physical inventories across all sites, so running leaner for counting purposes.”

The six industries reporting an increase in inventories in June — in the following order — are: Mining; Professional, Scientific & Technical Services; Information; Health Care & Social Assistance; Retail Trade; and Wholesale Trade. The seven industries reporting a decrease in inventories in June — in the following order — are: Other Services; Finance & Insurance; Construction; Educational Services; Management of Companies & Support Services; Public Administration; and Utilities.

Prices paid by services organizations for materials and services increased in June for the 109th consecutive month. The Prices Index registered 67.7 percent, a decrease of 3.6 percentage points from May’s reading of 71.3 percent, maintaining its 12-month average reading at 68 percent.

Sixteen industries reported an increase in prices paid during the month of June, in the following order: Accommodation & Food Services; Wholesale Trade; Construction; Other Services; Public Administration; Professional, Scientific & Technical Services; Information; Educational Services; Finance & Insurance; Arts, Entertainment & Recreation; Real Estate, Rental & Leasing; Mining; Transportation & Warehousing; Health Care & Social Assistance; Utilities; and Management of Companies & Support Services. No industries reported a decrease in prices paid.

The ISM® Services Backlog of Orders Index registered 54.9 percent, a 3.6-percentage point increase compared to the 51.3 percent reported in May and its highest level since February (55.9 percent). The index has been in expansion territory for five straight months. Of the total respondents in June, 29 percent indicated they do not measure backlog of orders. Respondent comments include: “Summer travel season has commenced” and “Data center work.”

The eight industries reporting an increase in order backlogs in June — in the following order — are: Real Estate, Rental & Leasing; Other Services; Accommodation & Food Services; Finance & Insurance; Professional, Scientific & Technical Services; Educational Services; Transportation & Warehousing; and Wholesale Trade. The seven industries reporting a decrease in order backlogs in June — in the following order — are: Agriculture, Forestry, Fishing & Hunting; Mining; Management of Companies & Support Services; Information; Construction; Utilities; and Health Care & Social Assistance.

Orders and requests for services and other non-manufacturing activities to be provided outside of the U.S. by domestically based companies expanded in June. The New Export Orders Index registered 50.4 percent, up 0.4 percentage point compared to the May reading of 50 percent. Of the total respondents in June, 40 percent indicated they do not perform, or do not separately measure, orders for work outside of the U.S. Respondent comments include: “Mainly driven by Latin America and Europe” and “Lower cost products are in higher demand.”

The three industries reporting an increase in new export orders in June are: Arts, Entertainment & Recreation; Mining; and Professional, Scientific & Technical Services. The five industries reporting a decrease in new export orders in June are: Construction; Health Care & Social Assistance; Finance & Insurance; Utilities; and Accommodation & Food Services. Ten industries reported no change in exports in June.

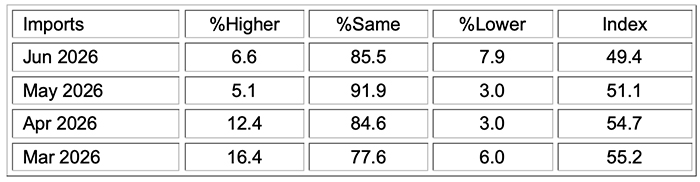

The Imports Index dropped into contraction territory in June after four months in expansion, registering 49.4 percent, 1.7 percentage points lower than the 51.1 percent reported in May. Of the total respondents in June, 36 percent reported that they do not use, or do not track the use of, imported materials. Respondent comments include: “Imports were not down in volume terms but became significantly more expensive, especially energy-linked imports, due to the U.S.-Iran war; hoping the cost of imports will decrease in the coming weeks (after the ceasefire)” and “Sourcing more equipment regionally to mitigate costs of tariffs.”

The five industries reporting an increase in imports for the month of June are: Arts, Entertainment & Recreation; Transportation & Warehousing; Professional, Scientific & Technical Services; Accommodation & Food Services; and Wholesale Trade. The four industries reporting a decrease in imports in June are: Other Services; Educational Services; Management of Companies & Support Services; and Health Care & Social Assistance. Nine industries reported no change in imports in June.

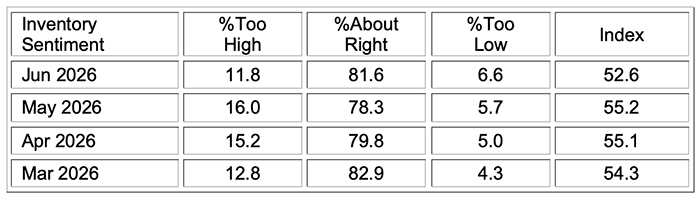

The ISM® Services Inventory Sentiment Index was in expansion (or “too high”) territory for the 38th consecutive month in June; the reading of 52.6 percent is a decrease of 2.6 percentage points compared to May’s figure of 55.2 percent. This reading indicates that respondents feel their companies’ inventory levels are too high when correlated to business requirements.

The nine industries reporting sentiment that their inventories were too high in June, in order, are: Other Services; Mining; Wholesale Trade; Accommodation & Food Services; Agriculture, Forestry, Fishing & Hunting; Retail Trade; Construction; Utilities; and Health Care & Social Assistance. The two industries reporting a decrease in inventory sentiment in June are: Finance & Insurance; and Professional, Scientific & Technical Services. Seven industries reported no change in inventory sentiment in June.

DO NOT CONFUSE THIS NATIONAL REPORT with the various regional purchasing reports released across the country. The national report’s information reflects the entire U.S., while the regional reports contain primarily regional data from their local vicinities. Also, the information in the regional reports is not used in calculating the results of the national report. The information compiled in this report is for the month of June 2026.

The data presented herein is obtained from a survey of supply executives in the services sector based on information they have collected within their respective organizations. ISM® makes no representation, other than that stated within this release, regarding the individual company data collection procedures. The data should be compared to all other economic data sources when used in decision-making.

The ISM® Services PMI® Report (formerly the Non-Manufacturing ISM® Report On Business®) is based on data compiled from purchasing and supply executives nationwide. Membership of the Services Business Survey Panel (formerly Non-Manufacturing Business Survey Committee) is diversified by the North American Industry Classification System (NAICS), based on each industry’s contribution to gross domestic product (GDP). The Services Business Survey Panel responses are divided into the following NAICS code categories: Agriculture, Forestry, Fishing & Hunting; Mining; Utilities; Construction; Wholesale Trade; Retail Trade; Transportation & Warehousing; Information; Finance & Insurance; Real Estate, Rental & Leasing; Professional, Scientific & Technical Services; Management of Companies & Support Services; Educational Services; Health Care & Social Assistance; Arts, Entertainment & Recreation; Accommodation & Food Services; Public Administration; and Other Services (services such as Equipment & Machinery Repairing; Promoting or Administering Religious Activities; Grantmaking; Advocacy; and Providing Dry-Cleaning & Laundry Services, Personal Care Services, Death Care Services, Pet Care Services, Photofinishing Services, Temporary Parking Services, and Dating Services). The data are weighted based on each industry’s contribution to GDP. According to U.S. Bureau of Economic Analysis (BEA) estimates (the average of the fourth quarter 2024 GDP estimate and the GDP estimates for first, second, and third quarter 2025, as released on January 22, 2026), the six largest services sectors are: Real Estate, Rental & Leasing; Public Administration; Professional, Scientific, & Technical Services; Health Care & Social Assistance; Information; and Finance & Insurance.

Survey responses reflect the change, if any, in the current month compared to the previous month. For each of the indicators measured (Business Activity, New Orders, Backlog of Orders, New Export Orders, Inventory Change, Inventory Sentiment, Imports, Prices, Employment and Supplier Deliveries), this report shows the percentage reporting each response and the diffusion index. Responses represent raw data and are never changed. Data is seasonally adjusted for Business Activity, New Orders, Prices and Employment. All seasonal adjustment factors are subject annually to relatively minor changes when conditions warrant them. The remaining indexes have not indicated significant seasonality.

The Services PMI® is a composite index based on the diffusion indexes for four of the indicators with equal weights: Business Activity (seasonally adjusted), New Orders (seasonally adjusted), Employment (seasonally adjusted) and Supplier Deliveries. Diffusion indexes have the properties of leading indicators and are convenient summary measures showing the prevailing direction of change and the scope of change. An index reading above 50 percent indicates that the services economy is generally expanding; below 50 percent indicates that it is generally declining. Supplier Deliveries is an exception. A Supplier Deliveries Index above 50 percent indicates slower deliveries and below 50 percent indicates faster deliveries.

A Services PMI® above 48.1 percent, over time, indicates that the overall economy, or gross domestic product (GDP), is generally expanding; below 48.1 percent, it is generally declining. The distance from 50 percent or 48.1 percent is indicative of the strength of the expansion or decline.

The ISM® Services PMI® Report survey is sent out to Services Business Survey Panel respondents in the first part of each month. Respondents are asked to ONLY report on U.S. operations for the current month. ISM® receives survey responses throughout most of any given month, with the majority of respondents generally waiting until late in the month to submit responses to give the most accurate picture of current business activity. ISM® then compiles the report for release on the third business day of the following month.

The industries reporting growth, as indicated in the ISM® Services PMI® Report, are listed in the order of most growth to least growth. For the industries reporting contraction or decreases, those are listed in the order of the highest level of contraction/decrease to the least level of contraction/decrease.

ISM PMI® Content

The Institute for Supply Management® (“ISM®”) PMI® Reports, formerly Report On Business®, (Manufacturing and Services reports) (“ISM PMI®”) contain information, text, files, images, video, sounds, musical works, works of authorship, applications, and any other materials or content (collectively, “Content”) of ISM (“ISM PMI® Content”). ISM PMI® Content is protected by copyright, trademark, trade secret, and other laws, and as between you and ISM, ISM owns and retains all rights in the ISM PMI® Content. ISM hereby grants you a limited, revocable, nonsublicensable license to access and display on your individual device the ISM PMI® Content (excluding any software code) solely for your personal, non-commercial use. The ISM PMI® Content shall also contain Content of users and other ISM licensors. Except as provided herein or as explicitly allowed in writing by ISM, you shall not copy, download, stream, capture, reproduce, duplicate, archive, upload, modify, translate, publish, broadcast, transmit, retransmit, distribute, perform, display, sell, or otherwise use any ISM PMI® Content.

Except as explicitly and expressly permitted by ISM, you are strictly prohibited from creating works or materials (including but not limited to tables, charts, data streams, time-series variables, fonts, icons, link buttons, wallpaper, desktop themes, online postcards, montages, mashups and similar videos, greeting cards, and unlicensed merchandise) that derive from or are based on the ISM PMI® Content. This prohibition applies regardless of whether the derivative works or materials are sold, bartered or given away. You shall not either directly or through the use of any device, software, internet site, web-based service, or other means remove, alter, bypass, avoid, interfere with or circumvent any copyright, trademark, or other proprietary notices marked on the Content or any digital rights management mechanism, device, or other content protection or access control measure associated with the Content including geo-filtering mechanisms. Without prior written authorization from ISM, you shall not build a business utilizing the Content, whether or not for profit.

You shall not create, recreate, distribute, incorporate in other work or advertise an index of any portion of the Content unless you receive prior written authorization from ISM. Requests for permission to reproduce or distribute ISM PMI® Content can be made by contacting in writing at: ISM Research, Institute for Supply Management, 350 W. Washington St. — Papago Gateway, Suite 301, Tempe, AZ 85288-1495, or by emailing kcahill@ismworld.org; Subject: Content Request.

ISM shall not have any liability, duty or obligation for or relating to the ISM PMI® Content or other information contained herein, any errors, inaccuracies, omissions or delays in providing any ISM PMI® Content or for any actions taken in reliance thereon. In no event shall ISM be liable for any special, incidental, or consequential damages arising out of the use of the ISM PMI®. Report On Business®, PMI®, Manufacturing PMI® and Services PMI® are registered trademarks of Institute for Supply Management®. Institute for Supply Management® and ISM® are registered trademarks of Institute for Supply Management, Inc.

About Institute for Supply Management®

Institute for Supply Management® (ISM®) is the first and leading not-for-profit professional supply management organization worldwide. Its community of more than 50,000 in more than 100 countries around the world manage about US$1 trillion in corporate and government supply chain procurement annually. Founded in 1915 by practitioners, ISM is committed to advancing the strategy and practice of integrated, end-to-end supply chain management through leading edge data-driven resources, community, and education to empower individuals, create organizational value and to drive competitive advantage. ISM’s vision is to foster a prosperous, sustainable world. ISM empowers and leads the profession through the ISM® PMI® Reports (formerly Report On Business®), its highly regarded certification and training programs, corporate services, events and assessments. The ISM® PMI® Reports — Manufacturing and Services — are two of the most reliable economic indicators available, providing guidance to supply management professionals, economists, analysts, and government and business leaders. For more information, please visit: https://www.ismworld.org.

The full text version of the ISM® Services PMI® Report is posted on ISM®’s website at www.ismrob.org on the third business day* of every month after 10:00 a.m. ET. The one exception is in January, the report is released on the fourth business day of the month.

The next ISM® Services PMI® Report featuring July 2026 data will be released at 10:00 a.m. ET on Wednesday, August 5, 2026.

*Unless the New York Stock Exchange is closed.

Forging the Next 250 Years: Powering the Next Era of American Manufacturing

As manufacturers offer more customization than ever before, managing product complexity has become a critical challenge. Tune in with Dan Joe Barry, Vice President of Product Marketing at Configit, who explores how companies are tackling the growing number of product configurations across engineering, sales, manufacturing, and service. He explains how Configuration Lifecycle Management (CLM) helps organizations maintain a single source of truth for configuration data. The result: fewer errors, faster quoting, and the ability to deliver customized products at scale.

Get In Touch

Google news and SEO compliant, Industry Today’s state-of-the-art digital media platform offers bespoke media campaigns that target key decision makers and buyers to achieve your marketing and promotional goals.

![]()

Contribute

Showcase your brand and promote your business to our highly targeted audience. We offer detailed Google Analytics with measurable ROI to assure success. Submit your content for review by our Editorial team who will contact you to discuss the project further.

About Us

Reach Your Targeted Audience and Grow Your Business. Learn more About Industry Today.

Contact Us

© 2026 Industry today. All Rights reserved.